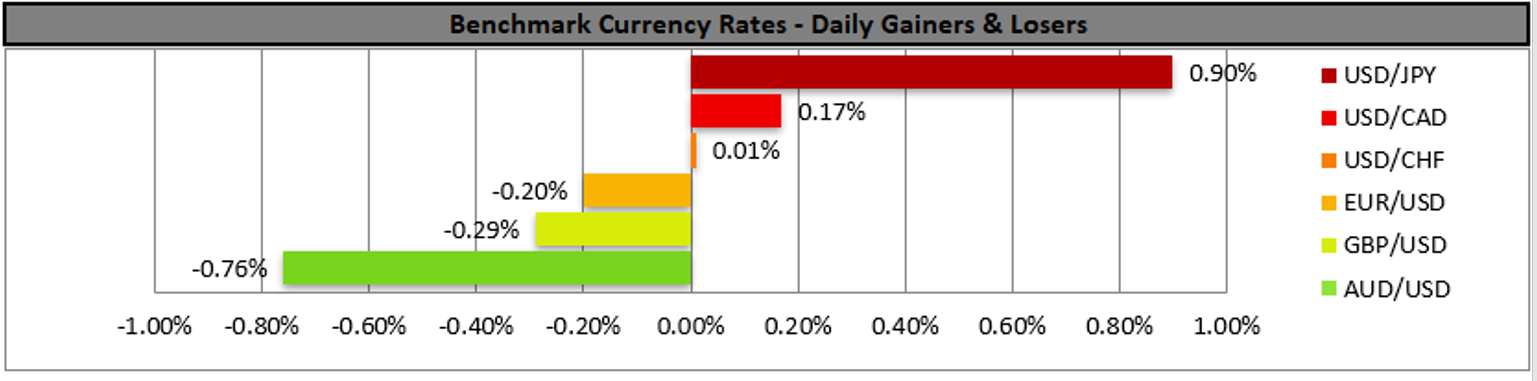

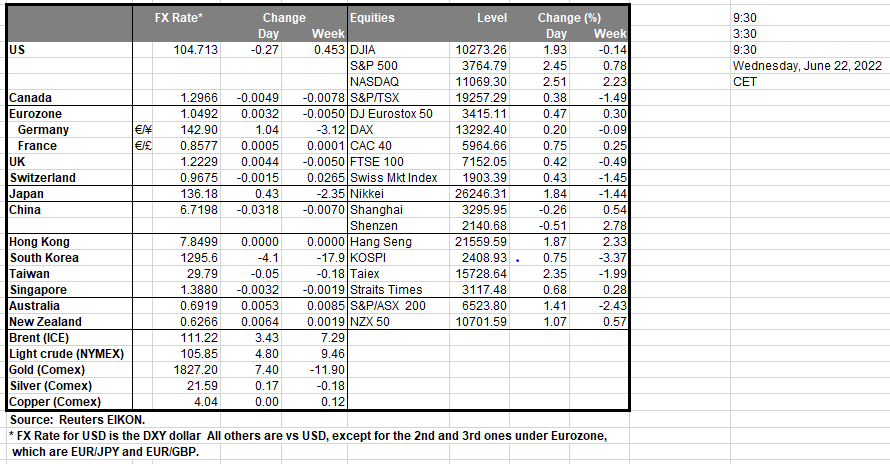

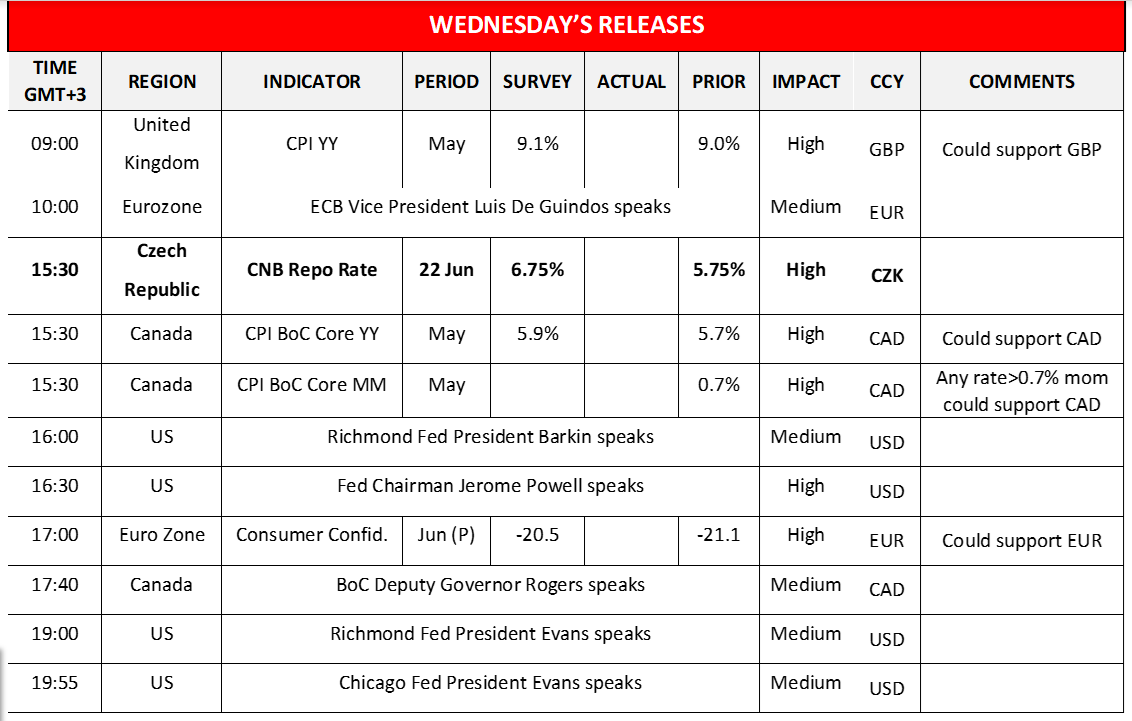

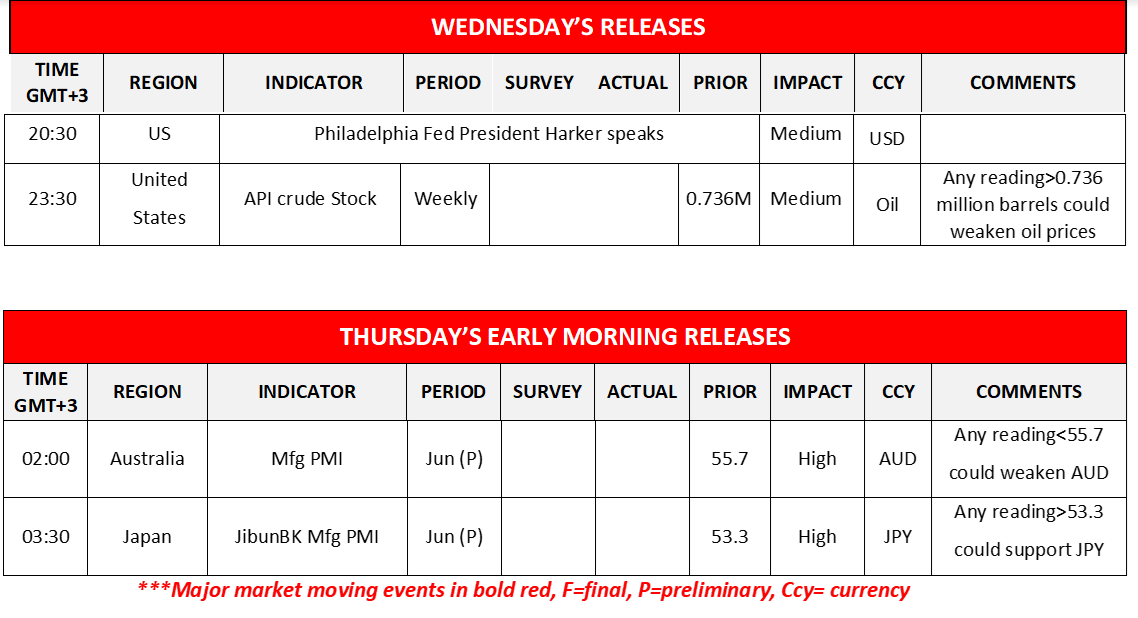

The USD tended to gain against a number of its counterparts yesterday as the US markets reopened after a long weekend, with maybe the most characteristic move being against the JPY as USD/JPY reached new twenty four year highs. It should be noted that the rise of US yields tended to provide additional support for the greenback, while at the same time the monetary outlook differentials of BoJ tended to weigh on the Japanese currency. On the monetary front we also note that Richmond Fed President Barkin add to the hawkish rhetoric of the Fed by reaffirming Fed Chairman Powell’s forward guidance for a 50 or 75 basis points rate hike in the next meeting, characterising it as reasonable. Today we highlight Fed Chairman Powell’s first testimony before Congress which is to be followed by a second one tomorrow, and should the Fed Chairman sound hawkish, given also his past forward guidance we may see the USD getting some support. At the same time US stockmarkets tended to rise as they tried to recover from a deep sell off last week yet all the main indexes for the US stockmarkets, Dow Jones, S&P 500 and Nasdaq started correcting lower during today’s Asian session. Also yesterday, Elon Musk stated that a recession in the near term is “more likely than not” while at the same time also stated that there are a few issues to be resolved for the Twitter deal, yet the statements did not seem to adversely affect the markets. No high impact financial releases are expected from the US today, yet we have a high number of Fed policymakers which are about to make statements and overall, we may see fundamentals leading the markets today. North of the US border though we get Canada’s CPI rates for May and a possible acceleration could provide some support for the Loonie as it could intensify the resolve of BoC to curb inflationary pressures with further rate hikes. CAD traders on the other hand may also pay close attention to BoC Deputy Governor Roger’s speech later today for any clues about the bank’s intentions. Similarly, across the pond, we also expect the release of UK’s CPI rates for May and a possible acceleration may induce BoE to widen its rate hikes instead the usual 25 basis points rate hikes it performs, which may provide some support for the pound today. We would also like to note from the Czech Republic CNB’s interest rate decision. The bank has been hiking rates and characteristically in the May meeting proceeded with a 75-basis points rate hike. Yet the CPI rate accelerated further in May reaching 16% yoy, a level not seen for over twenty-five years handling probably a shock to CNB policymakers. Today we would expect the bank to hike rates once again probably with a 100-basis points rate hike and at the same time remain substantially hawkish foreshadowing more rate hikes to come. Moving to the commodities front oil traders may keep an eye out for the API crude oil inventories figure and should the release show that US oil reserves rose substantially in the past week we may see oil prices slipping and vice versa.

本日はパウエルFRB議長の初の議会スピーチが行われ、明日には2回目のスピーチが行われる。パウエルFRB議長がタカ派的な発言をすれば、彼の過去のフォワードガイダンスも考慮すると、米ドルはいくらか上昇するかもしれない。 同時に、米国株式市場は、先週の激しい売りから回復しようとして上昇する傾向があったが、米国株式市場の主要指数であるダウ平均、S&P500、ナスダックは、今日のアジア時間中に下降修正し始めた。 昨日の欧州時間後半には、短期的な景気下落の可能性は「ないとは言えない」と述べ、同時にTwitterの取引について解決すべき問題がいくつかあると述べた。 今日は米国でインパクトの強い決算発表はないものの、多くのFRB政策担当者が発言を控えており、全体的にファンダメンタルズが相場を牽引する展開となりそうだ。 しかし、カナダでは5月の消費者物価指数が発表され、インフレ圧力を抑制するために追加利上げを行うBoCの決意が強まるため、カナダドルの上昇材料になるだろう。一方、カナダドル投資家は、ロジャーBoC副総裁のスピーチに注目し、BoCの意図について何か手がかりを得ることができるかもしれない。

同様に、英国でも5月の消費者物価指数の発表が予定されており、加速するであろうことから、BOEは通常の25bpの利上げから利上げ幅を拡大する可能性があり、これが今日のポンドの上昇材料となるだろう。 また、チェコ共和国CNBの金利決定にも注目したい。同銀行は利上げを続けており、5月の会合では特徴的に100bpの利上げを進めた。しかし、5月の消費者物価指数は前年同月比16%とさらに加速し、25年以上ぶりの水準となり、CNBの政策担当者に衝撃を与えたと思われる。本日は、おそらく100bpの利上げを実施し、同時にさらなる利上げを予感させる実質的なタカ派姿勢を維持すると予想される。 原油投資家はAPI原油在庫の数値に注目し、この発表で米国の原油備蓄が過去1週間で大幅に増加したことが明らかになれば、原油価格が下落する可能性がある。

USD/JPY 4時間チャート

Support: 135.20 (S1), 133.50 (S2), 132.30 (S3)

Resistance: 136.70 (R1), 138.00 (R2), 139.50 (R3)

GBP/USD 4時間チャート

Support: 1.2160 (S1), 1.2015 (S2), 1.1880 (S3)

Resistance: 1.2300 (R1), 1.2425 (R2), 1.2590 (R3)

もしこの記事に関して一般的なご質問やコメントがある場合は、reseach_team@ironfx.com宛で弊社のリサーチチームへ直接メールで連絡してください。 research_team@ironfx.com

免責事項:

本情報は、投資助言や投資推奨ではなく、マーケティングの一環として提供されています。IronFXは、ここで参照またはリンクされている第三者によって提供されたいかなるデータまたは情報に対しても責任を負いません。