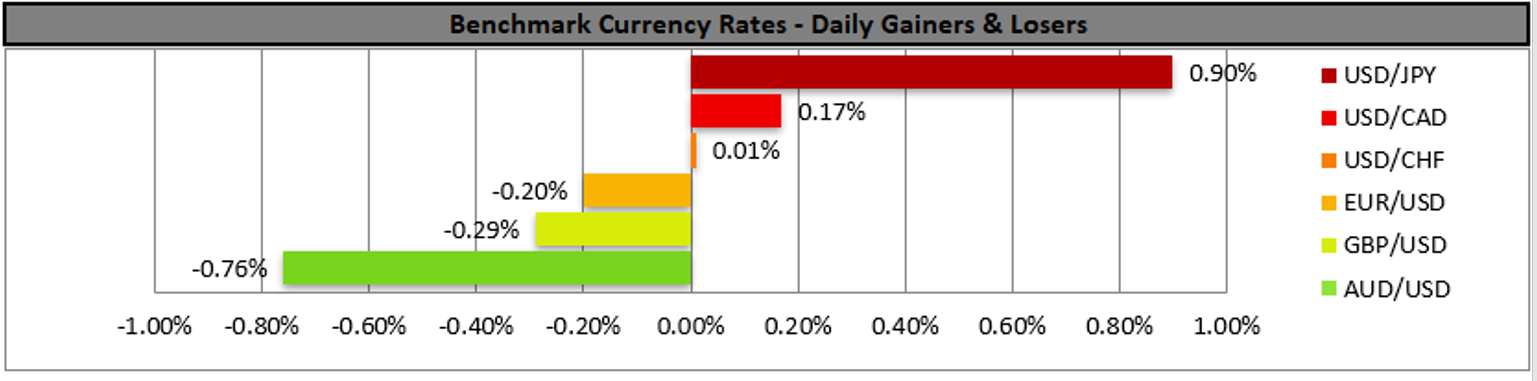

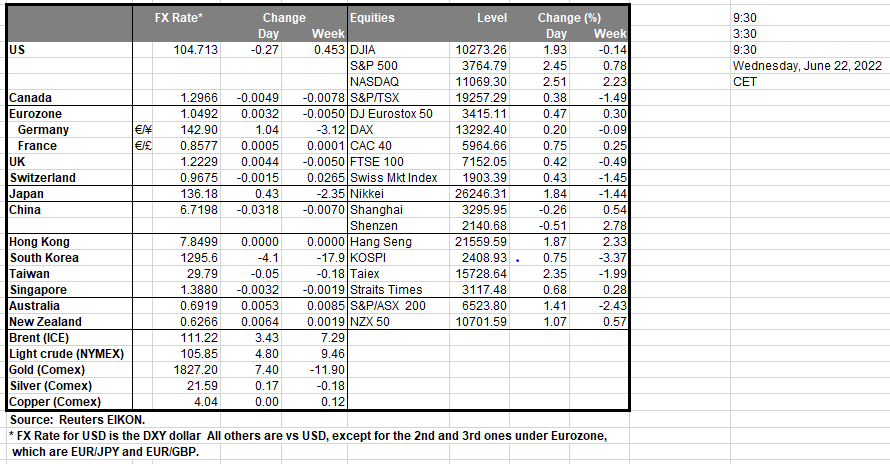

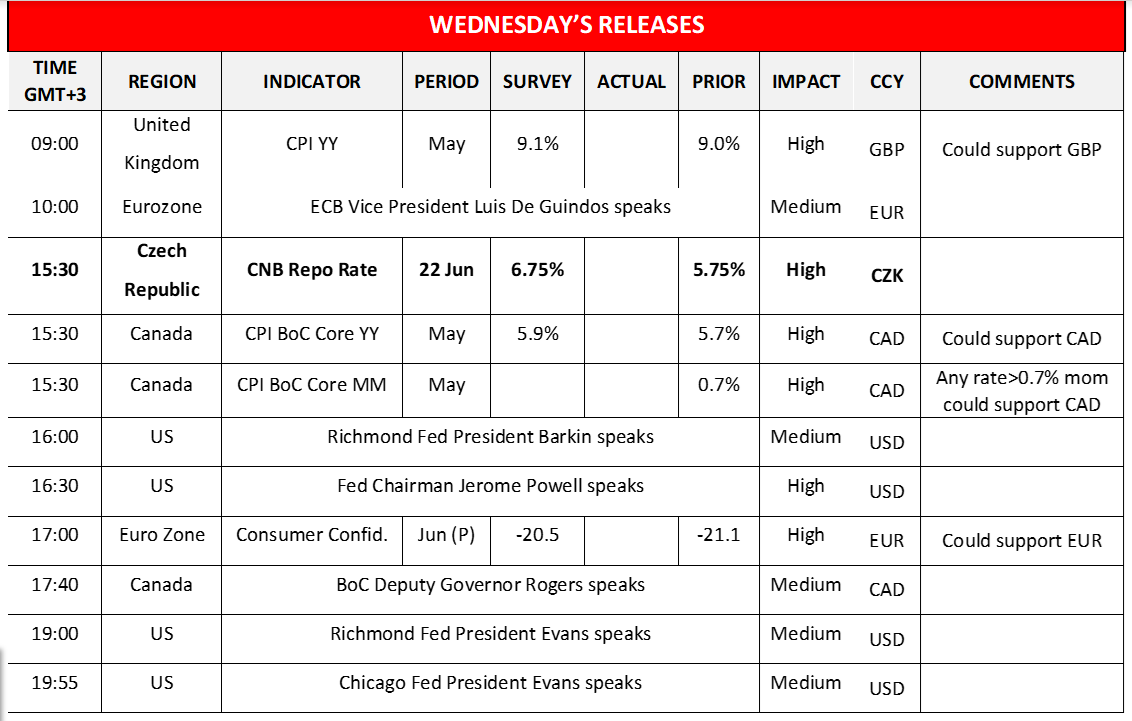

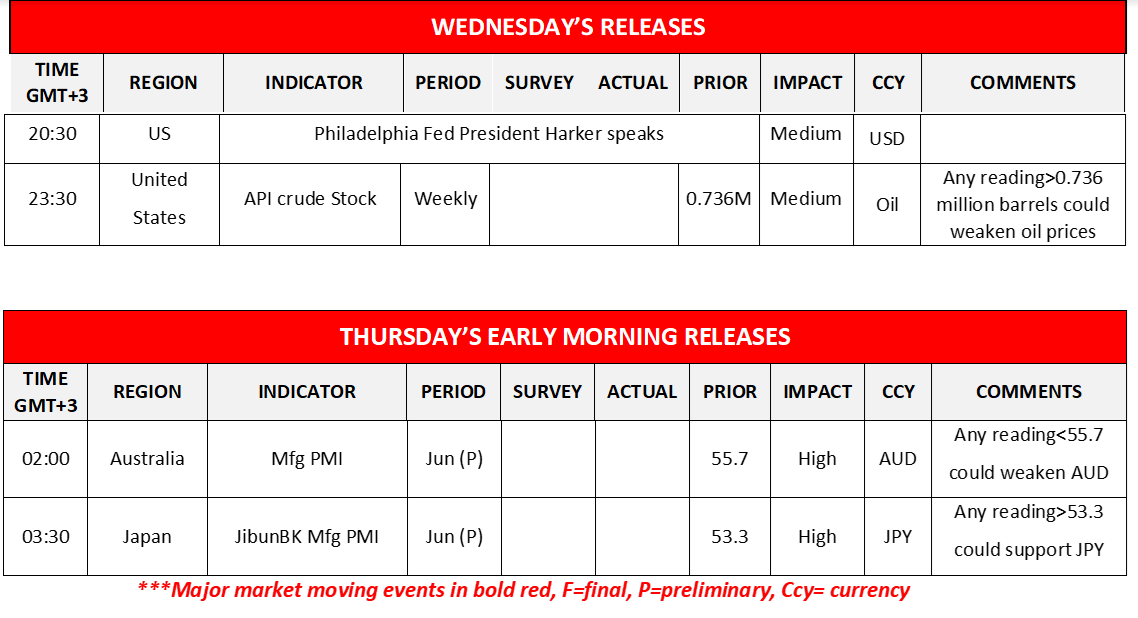

The USD tended to gain against a number of its counterparts yesterday as the US markets reopened after a long weekend, with maybe the most characteristic move being against the JPY as USD/JPY reached new twenty four year highs. It should be noted that the rise of US yields tended to provide additional support for the greenback, while at the same time the monetary outlook differentials of BoJ tended to weigh on the Japanese currency. On the monetary front we also note that Richmond Fed President Barkin add to the hawkish rhetoric of the Fed by reaffirming Fed Chairman Powell’s forward guidance for a 50 or 75 basis points rate hike in the next meeting, characterising it as reasonable. Today we highlight Fed Chairman Powell’s first testimony before Congress which is to be followed by a second one tomorrow, and should the Fed Chairman sound hawkish, given also his past forward guidance we may see the USD getting some support. At the same time US stockmarkets tended to rise as they tried to recover from a deep sell off last week yet all the main indexes for the US stockmarkets, Dow Jones, S&P 500 and Nasdaq started correcting lower during today’s Asian session. Also yesterday, Elon Musk stated that a recession in the near term is “more likely than not” while at the same time also stated that there are a few issues to be resolved for the Twitter deal, yet the statements did not seem to adversely affect the markets. No high impact financial releases are expected from the US today, yet we have a high number of Fed policymakers which are about to make statements and overall, we may see fundamentals leading the markets today. North of the US border though we get Canada’s CPI rates for May and a possible acceleration could provide some support for the Loonie as it could intensify the resolve of BoC to curb inflationary pressures with further rate hikes. CAD traders on the other hand may also pay close attention to BoC Deputy Governor Roger’s speech later today for any clues about the bank’s intentions. Similarly, across the pond, we also expect the release of UK’s CPI rates for May and a possible acceleration may induce BoE to widen its rate hikes instead the usual 25 basis points rate hikes it performs, which may provide some support for the pound today. We would also like to note from the Czech Republic CNB’s interest rate decision. The bank has been hiking rates and characteristically in the May meeting proceeded with a 75-basis points rate hike. Yet the CPI rate accelerated further in May reaching 16% yoy, a level not seen for over twenty-five years handling probably a shock to CNB policymakers. Today we would expect the bank to hike rates once again probably with a 100-basis points rate hike and at the same time remain substantially hawkish foreshadowing more rate hikes to come. Moving to the commodities front oil traders may keep an eye out for the API crude oil inventories figure and should the release show that US oil reserves rose substantially in the past week we may see oil prices slipping and vice versa.

지난주 미 증시 내 과매도 심리가 완화되며 반발 매수세로 일정 상승하였고, 금일 아시아 장 중 미국 3대 주요 지수인 다우존스, S&P500, 나스닥 모두 상승하였습니다. 한편 가까운 시일내에 유럽 경제가 침체에 빠질 수 있다는 가능성이 제시되며 시장의 우려가 악화되었습니다. 한편 트위터 인수 관련 일부 문제 사안들이 해결 될 것으로 예상되는 가운데 시장 내 큰 변동성을 제공하지는 못하였습니다. 금일 주요 경제지표 발표가 부재한 가운데 금일 연준 관계자들의 발언이 시장 내 변동성을 제공 할 것으로 예상됩니다. 캐나다 5월 CPI는 전년 동월대비 오를 것으로 예상되며, BoC는 인플레이션 억제를 위해 금리인상을 가속화 할 것으로 보입니다. CAD트레이더들은 금일 캐나다 중앙은행 로저스 수석 부국장의 연설에 주목해야합니다. 이와 비슷한 방향으로 영국 5월 CPI도 동월대비 오를 것으로 예상되며, 인플레이션이 억제되지 않는다면 기존 25bp 인상보다 강력한 금리인상이 강행 될 여지가 있으며, 그럴 경우 GBP는 상승할 수 있습니다.

금일 체코 중앙은행의 기준금리 발표가 예정된 가운데 앞서 지난 회의를 통해 100bp 금리인상을 결정했었습니다. 한편 체코 5월 물가상승률이 전년대비 16%를 기록하며 25년만에 최고치를 기록하며 체코 중앙은행 관계자들에게 충격을 주었습니다. 시장은 체코중앙은행의 매파적인 기조 유지와 함께 추가적인 금리인상 (100bp)을 전망하고 있습니다. 금일 있을 API 주간 원유 재고 발표에서 지난 주와 비교하여 원유 재고량이 증가한다면 유가는 하락할 것이고, 만약 원유 재고량이 감소하였다면 유가는 상승할 것입니다.

USD/JPY 4시간 차트

지지선: 135.20 (S1), 133.50 (S2), 132.30 (S3)

저항선: 136.70 (R1), 138.00 (R2), 139.50 (R3)

GBP/USD 4시간 차트

지지선: 1.2160 (S1), 1.2015 (S2), 1.1880 (S3)

저항선: 1.2300 (R1), 1.2425 (R2), 1.2590 (R3)

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.