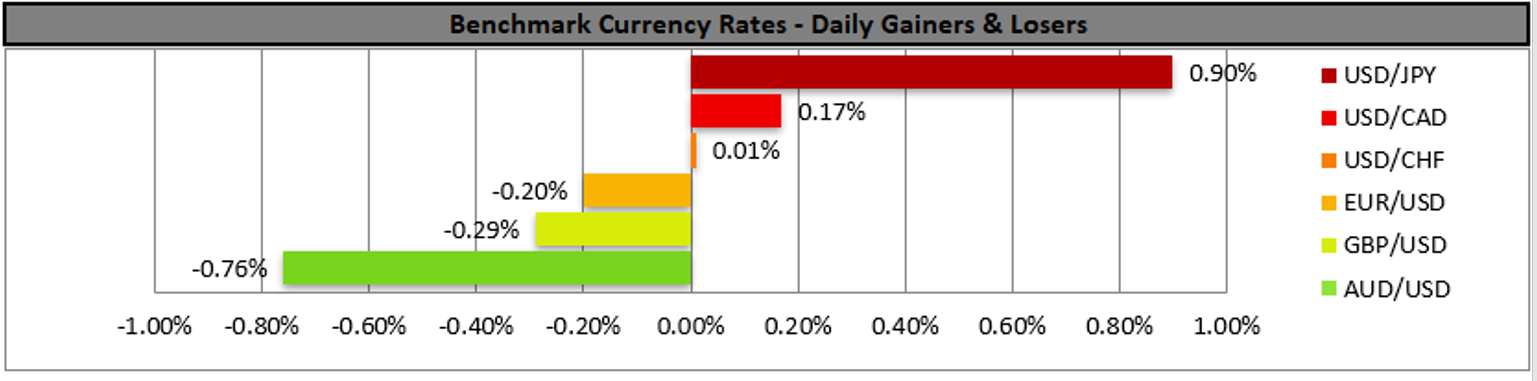

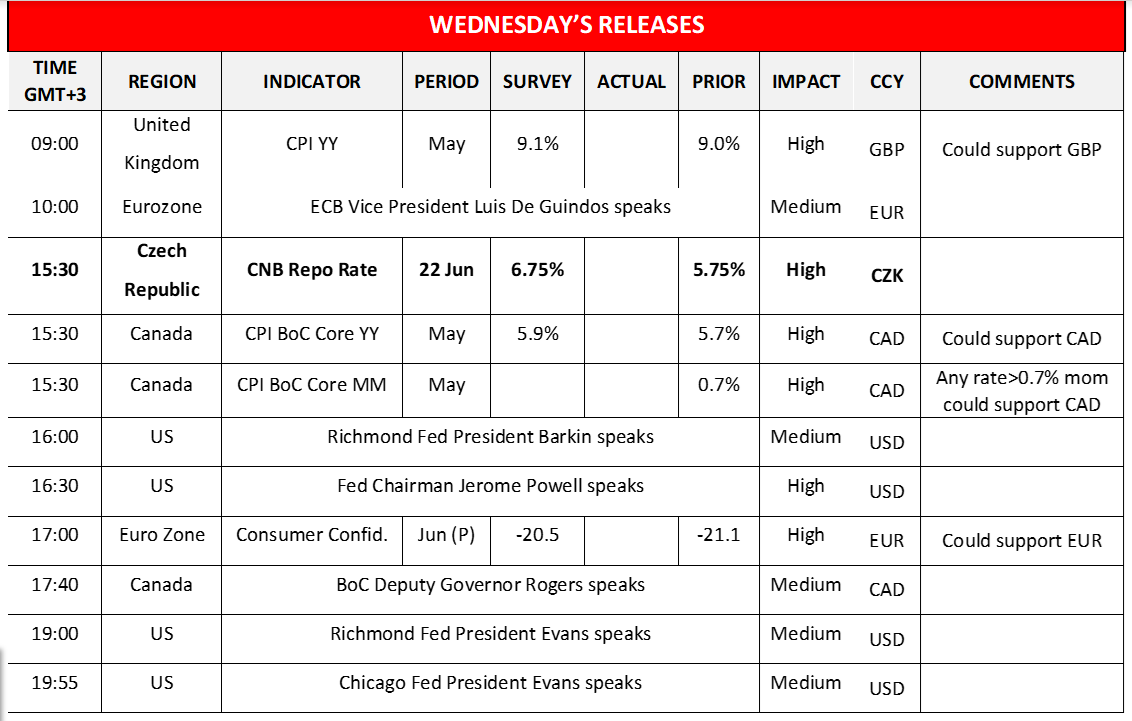

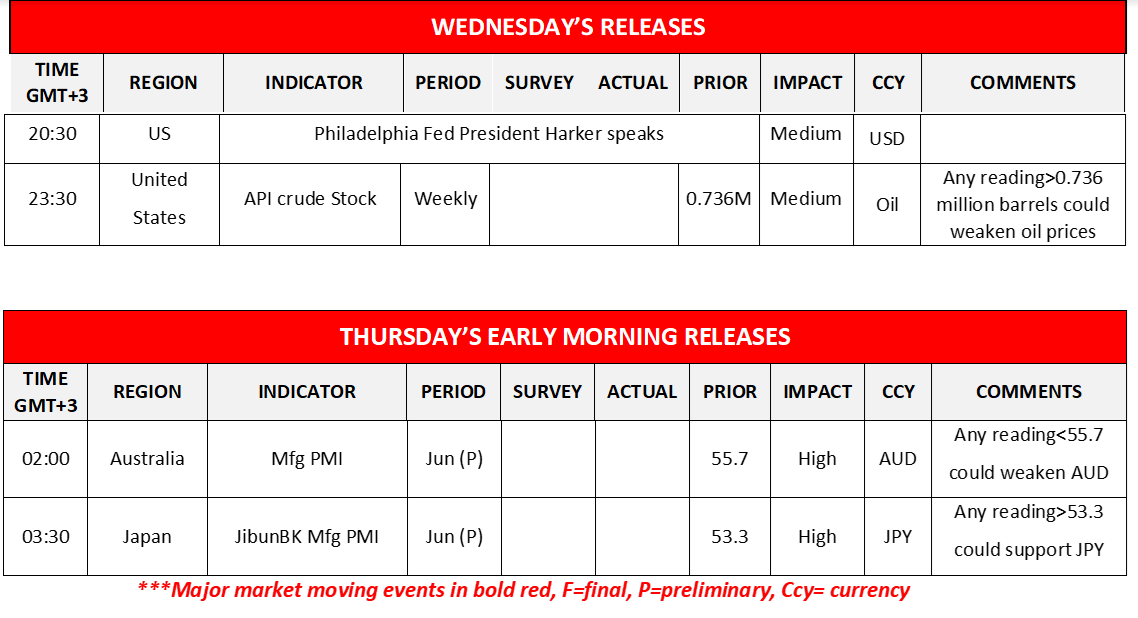

The USD tended to gain against a number of its counterparts yesterday as the US markets reopened after a long weekend, with maybe the most characteristic move being against the JPY as USD/JPY reached new twenty four year highs. It should be noted that the rise of US yields tended to provide additional support for the greenback, while at the same time the monetary outlook differentials of BoJ tended to weigh on the Japanese currency. On the monetary front we also note that Richmond Fed President Barkin add to the hawkish rhetoric of the Fed by reaffirming Fed Chairman Powell’s forward guidance for a 50 or 75 basis points rate hike in the next meeting, characterising it as reasonable. Today we highlight Fed Chairman Powell’s first testimony before Congress which is to be followed by a second one tomorrow, and should the Fed Chairman sound hawkish, given also his past forward guidance we may see the USD getting some support. At the same time US stockmarkets tended to rise as they tried to recover from a deep sell off last week yet all the main indexes for the US stockmarkets, Dow Jones, S&P 500 and Nasdaq started correcting lower during today’s Asian session. Also yesterday, Elon Musk stated that a recession in the near term is “more likely than not” while at the same time also stated that there are a few issues to be resolved for the Twitter deal, yet the statements did not seem to adversely affect the markets. No high impact financial releases are expected from the US today, yet we have a high number of Fed policymakers which are about to make statements and overall, we may see fundamentals leading the markets today. North of the US border though we get Canada’s CPI rates for May and a possible acceleration could provide some support for the Loonie as it could intensify the resolve of BoC to curb inflationary pressures with further rate hikes. CAD traders on the other hand may also pay close attention to BoC Deputy Governor Roger’s speech later today for any clues about the bank’s intentions. Similarly, across the pond, we also expect the release of UK’s CPI rates for May and a possible acceleration may induce BoE to widen its rate hikes instead the usual 25 basis points rate hikes it performs, which may provide some support for the pound today. We would also like to note from the Czech Republic CNB’s interest rate decision. The bank has been hiking rates and characteristically in the May meeting proceeded with a 75-basis points rate hike. Yet the CPI rate accelerated further in May reaching 16% yoy, a level not seen for over twenty-five years handling probably a shock to CNB policymakers. Today we would expect the bank to hike rates once again probably with a 100-basis points rate hike and at the same time remain substantially hawkish foreshadowing more rate hikes to come. Moving to the commodities front oil traders may keep an eye out for the API crude oil inventories figure and should the release show that US oil reserves rose substantially in the past week we may see oil prices slipping and vice versa.

Hoy destacamos el primer testimonio del presidente de la Fed, Powell, ante el Congreso, que será seguido por un segundo mañana, y si el presidente de la Fed se muestra agresivo, dada también su orientación a futuro anterior, podemos ver que el USD obtenga algo de apoyo. Al mismo tiempo, los mercados bursátiles de EE. UU. tendieron a subir mientras intentaban recuperarse de una venta masiva la semana pasada, pero todos los índices principales de los mercados bursátiles de EE. UU., Dow Jones, S&P 500 y Nasdaq comenzaron a corregir a la baja durante la sesión asiática de hoy. Durante la última sesión europea de ayer, Elon Musk declaró que una recesión en el corto plazo es "más probable que improbable", mientras que al mismo tiempo también afirmó que hay algunos problemas por resolver para el acuerdo de Twitter, sin embargo, las declaraciones no parecían afectar negativamente a los mercados. No se esperan publicaciones financieras de alto impacto de los EE. UU. hoy, pero tenemos un gran número de formuladores de políticas de la Fed que están a punto de hacer declaraciones y, en general, podemos ver los fundamentos liderando los mercados hoy. Al norte de la frontera con los EE. UU., aunque tenemos las tasas del IPC de Canadá para mayo, una posible aceleración podría brindar cierto apoyo al Loonie, ya que podría intensificar la determinación del BoC de frenar las presiones inflacionarias con más aumentos de tasas. Los comerciantes de CAD, por otro lado, también pueden prestar mucha atención al discurso del vicegobernador del BoC, Roger, más tarde hoy para obtener pistas sobre las intenciones del banco. Del mismo modo, al otro lado del charco, también esperamos la publicación de las tasas del IPC del Reino Unido para mayo y una posible aceleración puede inducir al BoE a ampliar sus aumentos de tasas en lugar de los habituales aumentos de tasas de 75 puntos básicos que realiza, lo que podría proporcionar cierto apoyo para la libra hoy.

También nos gustaría tomar nota de la decisión sobre la tasa de interés del CNB de la República Checa. El banco ha estado subiendo las tasas y, de manera característica, en la reunión de mayo procedió con un aumento de la tasa de 100 puntos básicos. Sin embargo, la tasa del IPC se aceleró aún más en mayo, alcanzando el 16 % interanual, un nivel que no se había visto en más de veinticinco años, lo que probablemente supuso un shock para los responsables de las políticas del CNB. Hoy esperaríamos que el banco suba las tasas una vez más, probablemente con una suba de tasas de 100 puntos básicos y, al mismo tiempo, se mantenga sustancialmente agresivo presagiando más alzas de tasas por venir. Pasando al frente de las materias primas, los comerciantes de petróleo pueden estar atentos a la cifra de inventarios de petróleo crudo API y, si la publicación muestra que las reservas de petróleo de EE. UU. aumentaron sustancialmente la semana pasada, podemos ver que los precios del petróleo caen y viceversa.

USD/JPY Gráfico 4H

Soporte: 135.20 (S1), 133.50 (S2), 132.30 (S3)

Resistencia: 136.70 (R1), 138.00 (R2), 139.50 (R3)

GBP/USD Gráfico 4H

Soporte: 1.2160 (S1), 1.2015 (S2), 1.1880 (S3)

Resistencia: 1.2300 (R1), 1.2425 (R2), 1.2590 (R3)

Si tiene usted alguna pregunta o comentario sobre este artículo, escriba un correo directamente a nuestro equipo de investigación research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.