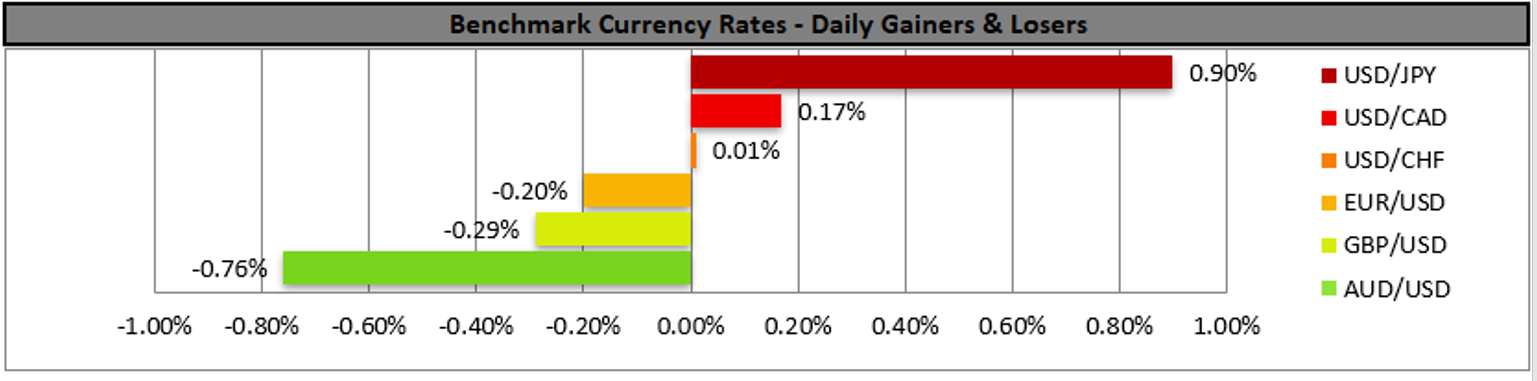

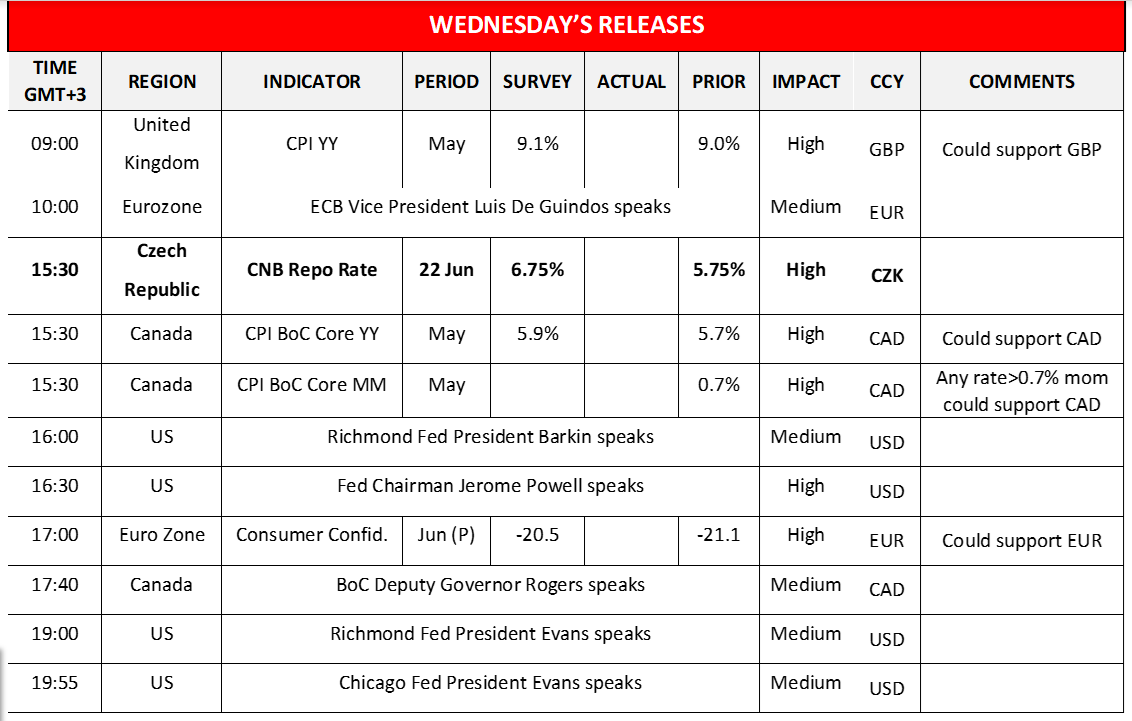

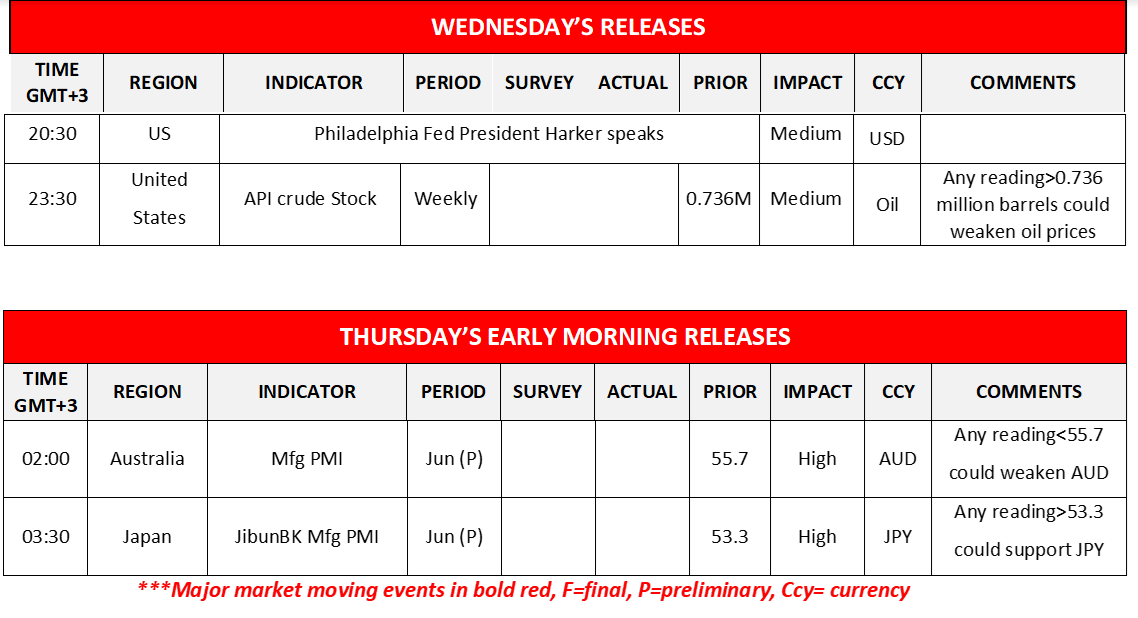

The USD tended to gain against a number of its counterparts yesterday as the US markets reopened after a long weekend, with maybe the most characteristic move being against the JPY as USD/JPY reached new twenty four year highs. It should be noted that the rise of US yields tended to provide additional support for the greenback, while at the same time the monetary outlook differentials of BoJ tended to weigh on the Japanese currency. On the monetary front we also note that Richmond Fed President Barkin add to the hawkish rhetoric of the Fed by reaffirming Fed Chairman Powell’s forward guidance for a 50 or 75 basis points rate hike in the next meeting, characterising it as reasonable. Today we highlight Fed Chairman Powell’s first testimony before Congress which is to be followed by a second one tomorrow, and should the Fed Chairman sound hawkish, given also his past forward guidance we may see the USD getting some support. At the same time US stockmarkets tended to rise as they tried to recover from a deep sell off last week yet all the main indexes for the US stockmarkets, Dow Jones, S&P 500 and Nasdaq started correcting lower during today’s Asian session. Also yesterday, Elon Musk stated that a recession in the near term is “more likely than not” while at the same time also stated that there are a few issues to be resolved for the Twitter deal, yet the statements did not seem to adversely affect the markets. No high impact financial releases are expected from the US today, yet we have a high number of Fed policymakers which are about to make statements and overall, we may see fundamentals leading the markets today. North of the US border though we get Canada’s CPI rates for May and a possible acceleration could provide some support for the Loonie as it could intensify the resolve of BoC to curb inflationary pressures with further rate hikes. CAD traders on the other hand may also pay close attention to BoC Deputy Governor Roger’s speech later today for any clues about the bank’s intentions. Similarly, across the pond, we also expect the release of UK’s CPI rates for May and a possible acceleration may induce BoE to widen its rate hikes instead the usual 25 basis points rate hikes it performs, which may provide some support for the pound today. We would also like to note from the Czech Republic CNB’s interest rate decision. The bank has been hiking rates and characteristically in the May meeting proceeded with a 75-basis points rate hike. Yet the CPI rate accelerated further in May reaching 16% yoy, a level not seen for over twenty-five years handling probably a shock to CNB policymakers. Today we would expect the bank to hike rates once again probably with a 100-basis points rate hike and at the same time remain substantially hawkish foreshadowing more rate hikes to come. Moving to the commodities front oil traders may keep an eye out for the API crude oil inventories figure and should the release show that US oil reserves rose substantially in the past week we may see oil prices slipping and vice versa.

در جلسه آخر وقت دیروز اتحادیه اروپا اعلام شد که رکود اقتصادی در کوتاه مدت "بیشتر محتمل" است، و در عین حال همچنین اظهار شد که چند موضوع برای معامله توییتر وجود دارد که باید حل شود، به نظر نمی رسد این اظهارات بر بازارها تأثیر منفی بگذارد. امروز انتظار نمیرود که انتشارات مالی با تأثیر زیاد از ایالات متحده منتشر شود، با این حال تعداد زیادی سیاستگذار فدرال رزرو وجود دارند که در شرف بیان اظهارات هستند و به طور کلی، ممکن است امروز شاهد عوامل بنیادی هدایتگر بازار بود.

در شمال مرز ایالات متحده، نرخهای شاخص قیمت مصرف کننده کانادا برای ماه مه دریافت خواهد شد و یک شتاب احتمالی میتواند تا حدودی از دلار کانادا حمایت کند، زیرا میتواند عزم بانک مرکزی کانادا برای مهار فشارهای تورمی با افزایش بیشتر نرخها را تشدید کند. از سوی دیگر، معامله گران دلار کانادا نیز ممکن است به سخنان راجر معاون رئیس بانک مرکزی این کشور در اواخر امروز برای هرگونه سرنخ در مورد نیات بانک توجه زیادی داشته باشند. به طور مشابه، در آن سوی اروپا، می توان همچنین انتظار داشت که نرخهای شاخص قیمت مصرف کننده بریتانیا برای ماه مه منتشر شوند و یک شتاب احتمالی ممکن است بانک مرکزی انگلستان را وادار کند که افزایش نرخ خود را بهجای افزایشهای معمول ۲۵ واحد پایه که انجام میدهد، انجام دهد، که ممکن است امروز تا حدی از پوند حمایت کند. همچنین باید از تصمیم بانک مرکزی جمهوری چک در مورد نرخ بهره یاد کرد. این بانک در حال افزایش نرخ بوده است و مشخصاً در جلسه ماه مه یکصد واحد پایه افزایش نرخ را انجام داد. با این حال، نرخ شاخص قیمت مصرف کننده در ماه مه شتاب بیشتری گرفت و به ۱۶ درصد سالانه رسید، سطحی که برای بیش از بیست و پنج سال دیده نشده بود و احتمالاً یک شوک برای سیاستگذاران بانک مرکزی جمهوری چک بود. امروز می توان انتظار داشت که بانک احتمالاً با افزایش ۱۰۰ واحدی نرخ بهره را بار دیگر افزایش دهد و در عین حال به طور قابل توجهی بازی باقی بماند که پیش بینی کننده افزایش نرخ های بیشتر در آینده است. در جبهه بازارهای کالا، معامله گران نفت خام می توانند مراقب رقم موجودی نفت خام مؤسسه نفت آمریکا باشند و اگر انتشار نشان دهد که ذخایر نفت ایالات متحده به میزان قابل توجهی در هفته گذشته افزایش یافته است، می توان شاهد کاهش قیمت نفت بود و بالعکس.

نمودار چهار ساعته دلار آمریکا / ین ژاپن

Support: 135.20 (S1), 133.50 (S2), 132.30 (S3)

Resistance: 136.70 (R1), 138.00 (R2), 139.50 (R3)

نماد چهار پوند به دلار امریکا

Support: 1.2160 (S1), 1.2015 (S2), 1.1880 (S3)

Resistance: 1.2300 (R1), 1.2425 (R2), 1.2590 (R3)

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.