USD remains steady as the week begins

The USD tended to remain relatively steady as the week begins. The FX market presents little volatility and with the absence of high impact US financial releases we expect fundamentals to lead the markets today. It should be noted though that the release of the US employment report for June is coming up on Thursday while for US markets the week is to be short, given the US public holiday on the 3rd of July. Also, US stock markets seem to present low volatility with the market’s eye still on the tech sector, while also gold’s price seems to stabilise somewhat, given also USD’s current inactivity.

Oil prices stabilise for now

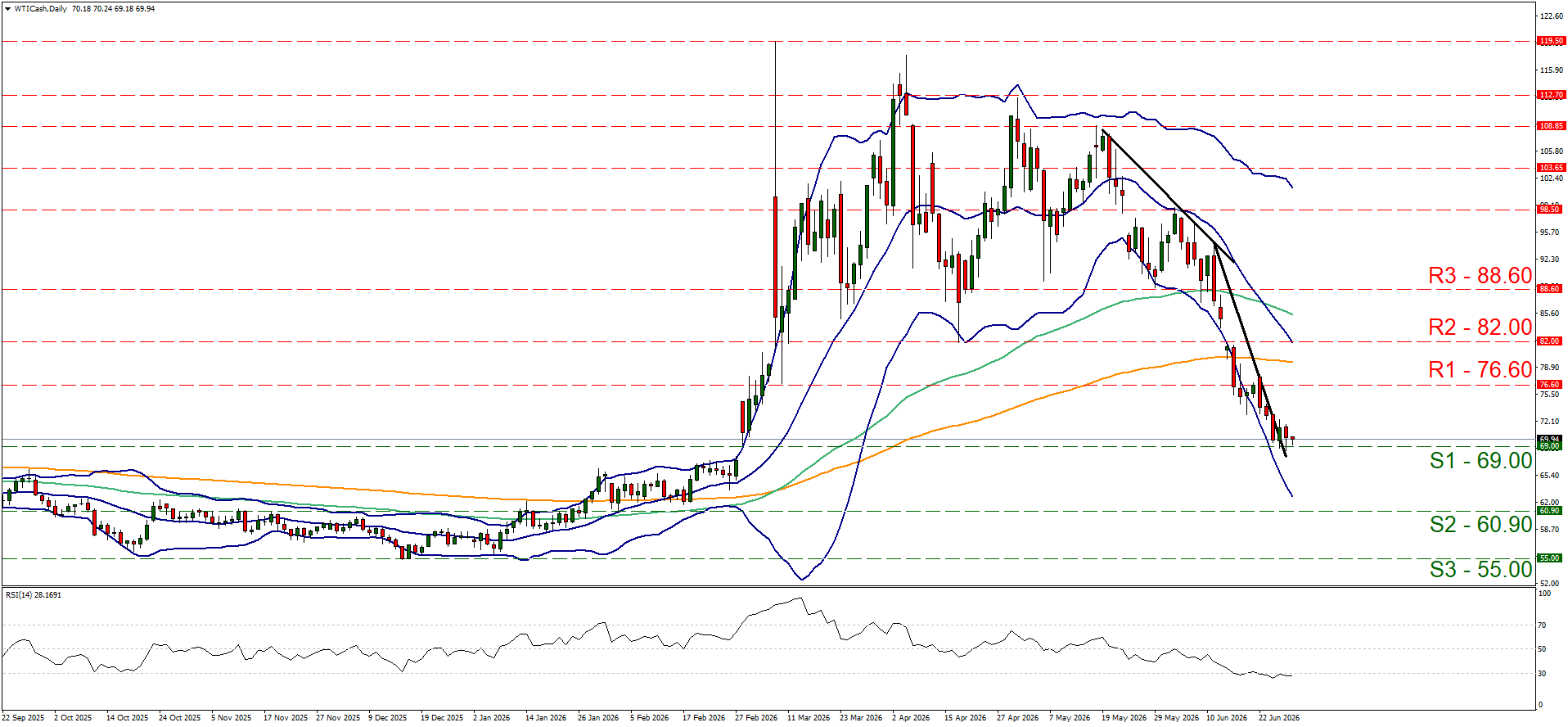

Oil prices tended to stabilise, with WTI being in the area of $69 per barrel. There seems some hesitation on behalf of the bears as minor tensions were present in the Persian Gulf. We still view the hesitation as temporary and we may see oil prices edging lower yet as mentioned in last week’s report, we expect them to land a bit higher than before the US-Iran crisis.

Other highlights for today

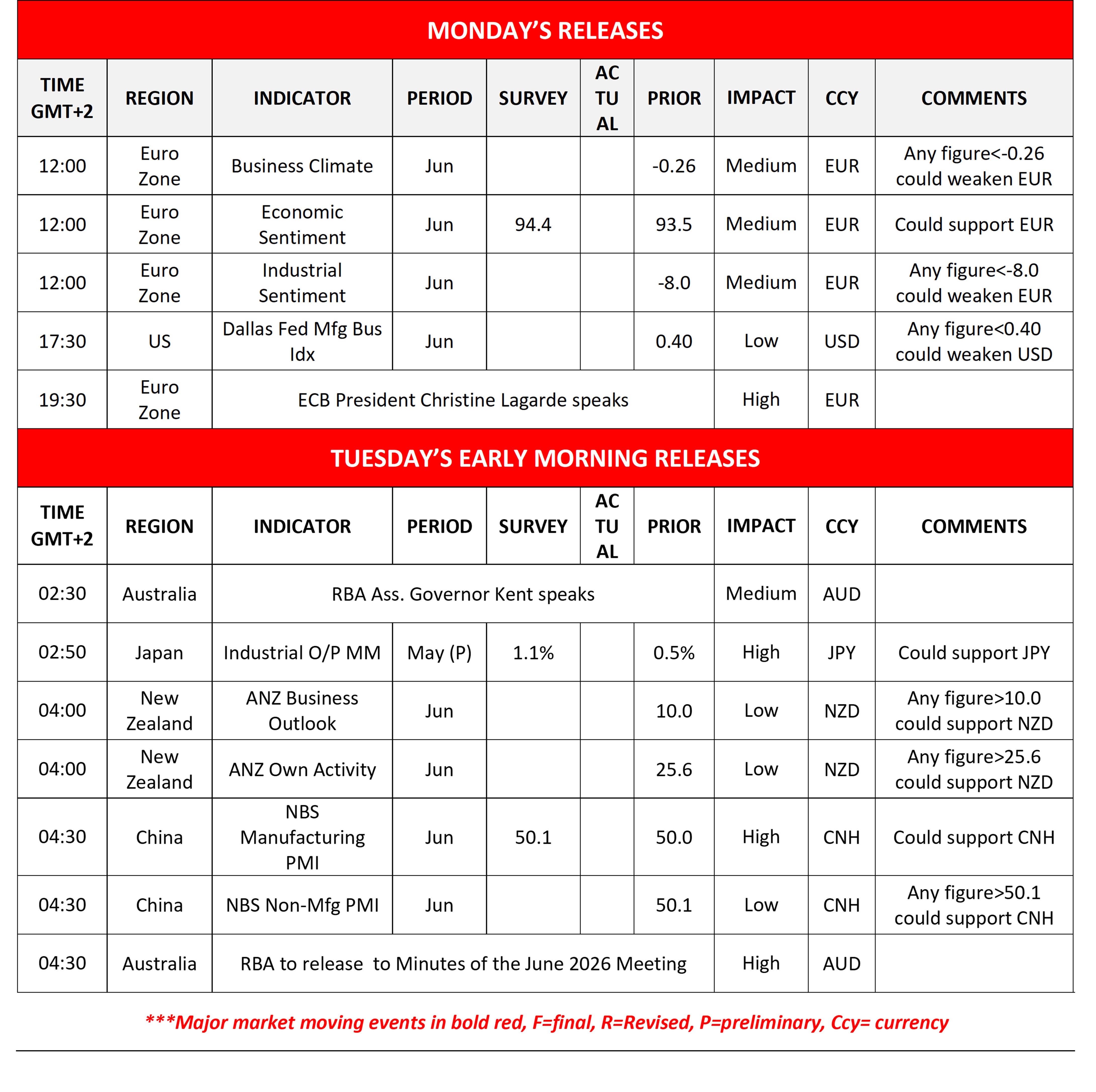

Today we get Euro Zone’s business climate indicators and the US Dallas Fed business index both for June, while ECB President Lagarde speaks. In tomorrow’s Asian session, we get Japan’s preliminary industrial output for May, New Zealand’s ANZ indicators for and China’s PMI figures for June, while RBA Ass. Governor Kent speaks and RBA is to release the June meeting minutes.

As for the rest of the week

On Tuesday we get UK’s GDP rates for Q1, France’s and Germany’s preliminary HICP Rates for June, Canada’s GDP rates for April and from the US the Consumer confidence for June and the JOLTS job openings for May. On Wednesday we get Japan’s Tankan indexes for Q2, China’s RatingDog manufacturing PMI figure for June, UK’s Nationwide house prices for June, Germanys’ final manufacturing PMI figure for June, Euro Zone’s preliminary HICP rates for June and from the US the ADP National Employment figure for June and the US ISM manufacturing PMI figure for June. On Thursday we get Switzerland’s CPI rates for June the US employment report for the same month, the US weekly initial jobless claims figure and the US factory orders for May. On Friday we get Turkey’s CPI rates for June and the final UK Services PMI figure for June, while in the US it’s a public holiday.

Charts to keep an eye out

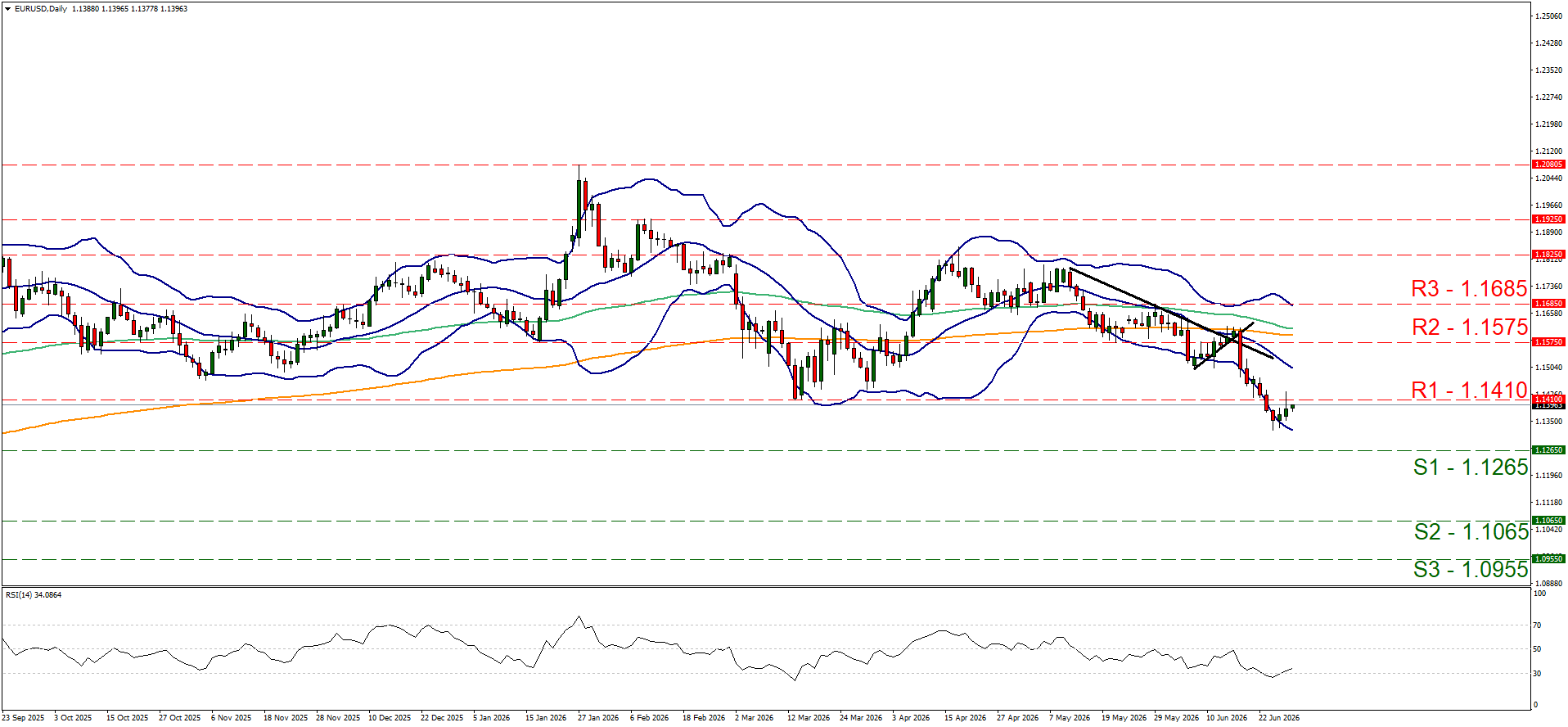

EUR/USD edged higher, mostly as a result of USD weakness rather than EUR strength, nearing the 1.1410 (R1) resistance line. The bearish market sentiment has eased yet seems to be still present given that the RSI indicator has risen yet is still close to the reading of 30. We tend to expect a stabilisation of the pair for the time being, yet view the USD as being in the driver’s seat for the pair. Should the bears regain control over EUR/USD direction we may see it aiming if not reaching the 1.1265 (S1) support line. Should the bulls take over, we may see the pair breaking the 1.1410 (R1) resistance level and start aiming for the 1.1575 (R2) level.

WTI’s price remained close to the 69.00 (S1) support line. WTI’s price seems to have broken the downward trendline and to have some difficulty breaking clearly the S1, hence we tend to maintain bias for the stabilisation of WTI’s price. Yet the RSI indicator has remained below the reading of 30, implying that the commodity’s price is still at oversold levels and may be ripe for a correction higher. Should the bears remain in charge of WTI’s direction, it could breach the 69.00 (S1) support line and start aiming for the 60.90 (S2) support level. Should the bulls take over, we may see the pair reversing direction, breaking the prementioned downward trendline and continue, higher aiming if not reaching the 76.60 (R1) resistance level.

EUR/USD Daily Chart

- Support: 1.1265 (S1), 1.1065 (S2), 1.0955 (S3)

- Resistance: 1.1410 (R1), 1.1575 (R2), 1.1685 (R3)

WTI Daily Chart

- Support: 69.00 (S1), 60.90 (S2), 55.00 (S3)

- Resistance: 76.60 (R1), 82.00 (R2), 88.60 (R3)

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.