The week is nearing its end and we have a look at what next week has in store for the markets. On Monday we get Japan’s final Jibunk manufacturing PMI figure and China’s Caixin final manufacturing PMI figure, followed by the UK’s nationwide house price rate, Germany’s HCOB manufacturing PMI figure and the UK’s manufacturing PMI figure all for the month of August and the Eurozone’s unemployment rate for July. On Tuesday we get the Eurozone’s preliminary HICP rate, Canada’s manufacturing PMI figure and the US ISM manufacturing PMI figure all for the month of August. On Wednesday, we get Australia’s GDP rate for Q2, China’s Caixin services PMI figure, Turkey’s CPI rate and France’s services PMI figure all for August, followed by the US’s factory orders rate and JOLTS Job openings figure both for July. On Thursday we get Australia’s trade balance figure for July, Sweden’s preliminary CPI rate ,Switzerland’s CPI rate, the Czech Republic’s preliminary CPI rate and the US ADP national employment figure all for the month of August, Canada’s trade balance figure for July and the US ISM non-manufacturing PMI figure for August. On Friday, we get Germany’s industrial orders rate for July, the UK’s Halifax house prices rate for August, the UK’s retail sales rate for July, the Eurozone’s revised GDP rate for Q2, the US Employment data for August, Canada’s employment data for August and Canada’s Ivey PMI figure for August.

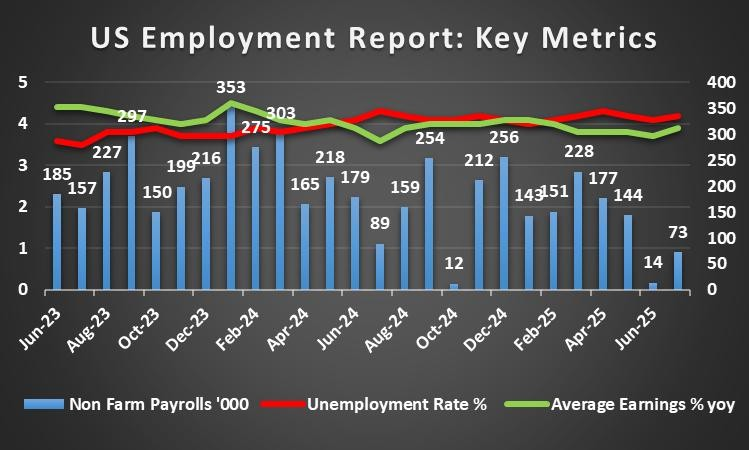

USD – Employment data next Friday

On a political level, President Trump earlier on this week “fired” Fed Board Governor Cook, following criminal allegations made against the Governor in regards to some of her mortgage applications. The firing of the Governor has sparked a debate and worries over the Fed’s independence, especially considering that they are simply allegations at this point. On a macroeconomic level, the US PCE rates are due out today and could significantly influence the narrative for the dollar heading into next week, yet a small uptick in inflationary pressures may not suffice to change the overall dovish narrative which emerged from Fed Chair Powell last Friday. Moreover, heading into next week, the US Employment data will be the main highlight for dollar traders as the Unemployment rate is expected to increase to 4.3%, which could prompt further calls for a Fed rate cut and could thus weigh on the dollar.

Analyst’s opinion (USD)

“In our view the Fed has had it’s “dovish” pivot following Powell’s comments last Friday. In turn we would not be surprised to see the Fed cutting rates in their next meeting even if the PCE rates today tick slightly upwards. Our main concern however is the legal battle which will ensure between Governor Cook and President Trump, as the Fed’s independence is crucial and the White House’s pre-emptive firing could set a dangerous precedent down the line and could reduce confidence in the US as a whole.”

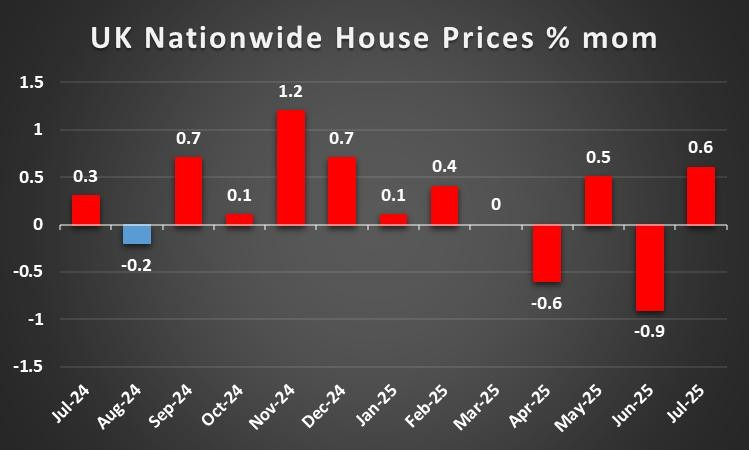

GBP – Manufacturing data next week for sterling traders

On a macroeconomic level, we note the release of the UK’s manufacturing PMI figure for August which is due out on Monday. Should the figure showcase an improvement or even enter expansionary territory it may be seen as a positive for the manufacturing sector of the UK economy and could possibly provide support for the sterling . On a monetary level, BoE Governor Bailey noted that Britain is facing a challenge from its weak underlying economic growth and drop in number of workers since the pandemic. Thus the concerns of the Governor in regards to the nation’s economic growth may imply that the bank could maintain its rate cutting approach in order to stimulate the economy.

Analyst’s opinion (GBP)

“The UK’s manufacturing data is interesting for pound traders, yet our main concern is the recent reports about the imposition of NIS contributions on rental income. Such a possibility could heavily influence the UK economy and thus may warrant closer attention.”

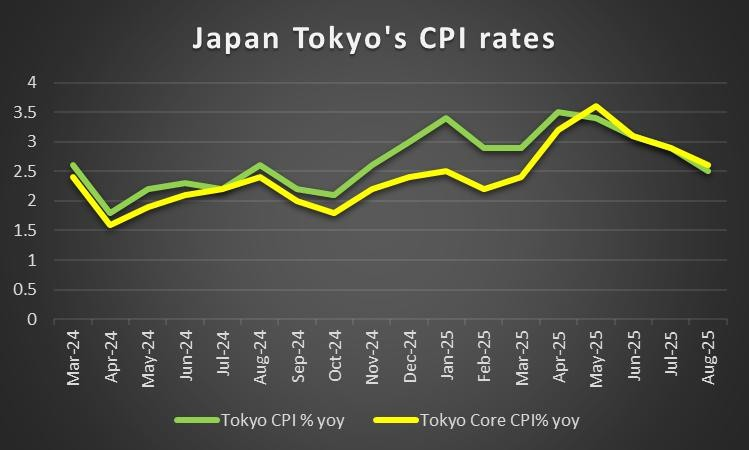

JPY – Japan’s Tokyo CPI rates come in lower than expected

For JPY traders on a macroeconomic level, we highlight the release of Japan’s Tokyo CPI rates for August earlier on today. Japan’s Tokyo CPI rates tended to confirm the expectations of economists in regards to easing inflationary pressures in the Japanese economy. In turn the implications of easing inflationary pressures in the Japanese economy may reduce calls for the BOJ to resume on their rate hiking path. Hence, should BOJ policymakers showcase an unwillingness to hike rates in the near future it may be perceived as dovish in nature which in turn could potentially weigh on the JPY. In terms of financial releases in the upcoming week, it’s set to be pretty easy going with no major financial releases expected from Japan, with only their JiBunk final manufacturing PMI figure for August being of high significance. On a monetary level we note the comments made by BOJ member Nakagawa who stated that “uncertainty surrounding trade policies have eased slightly compared to April” which could imply that the bank may be prepared to take financial releases at face value and reduce the incorporation of possible shocks as a result of the US’s trade ambitions into the bank’s considerations during their monetary policy meeting.

Analyst’s opinion (JPY)

“We don’t see the immediate case for the BOJ to resume on their rate hiking path. Specifically, the release of the Tokyo CPI rates today showcase once again that inflation appears to be moderating and thus there appears to be no need in our opinion for the BOJ to hike in their next meeting. Therefore, the JPY’s direction in the coming week may be dictated by other stronger currencies”

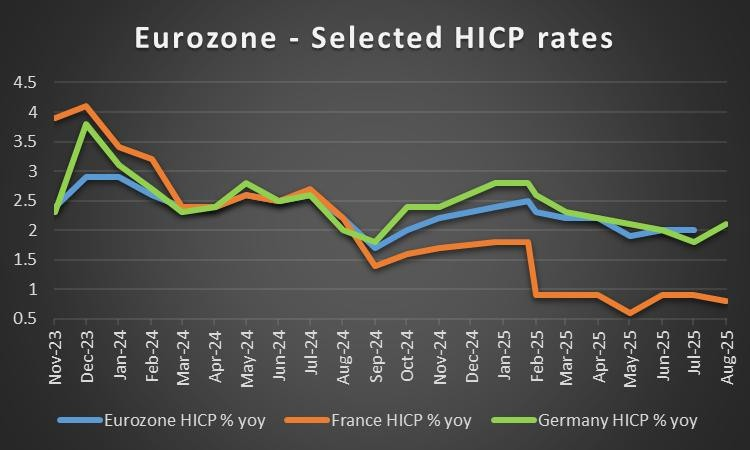

EUR – EU GDP rates next week

On a macroeconomic and monetary level, it was a busy week for EUR traders with the release of Germany’s and France’s preliminary HICP rates earlier on today and the release of the ECB’s last meeting minutes. Starting with the ECB’s July meeting minutes in which it was stated that “Indicators of underlying inflation were consistent overall with the 2% medium- term target” implying that the bank is not in a rush to cut rates and thus could opt for a more gradual rate cutting approach or even possibly remain on hold in the near future. In turn this may have provided support for the EUR. Interestingly France’s preliminary HICP rate for August came in lower than expected and thus should Germany’s preliminary HICP rate for August which at the time of this report have not been released, showcase easing inflationary pressures it could weigh on the EUR. For next week EUR traders may be looking forward to the Zone’s revised GDP rate for Q2 as well as the Zone’s preliminary HICP rate for August. Both financial releases could dictate the ECB’s stance heading into September. On a political level, France is once again in political turmoil with possible early elections occuring on the 8th of September. The political instability could possibly weigh on the European Equities markets.

Analyst’s opinion (EUR)

“France’s political turmoil is counterproductive for the rest of the Zone. The political issues in France need to be resolved overall in our opinion. Moving on, the ECB appears to have no reason to rush to cut rates and thus we wouldn’t be surprised to see them remaining on hold given that inflation appears to be easing and the EUR’s levels against the dollar from an FX perspective have improved and thus could counter inflationary pressures as noted in the bank’s July meeting minutes”

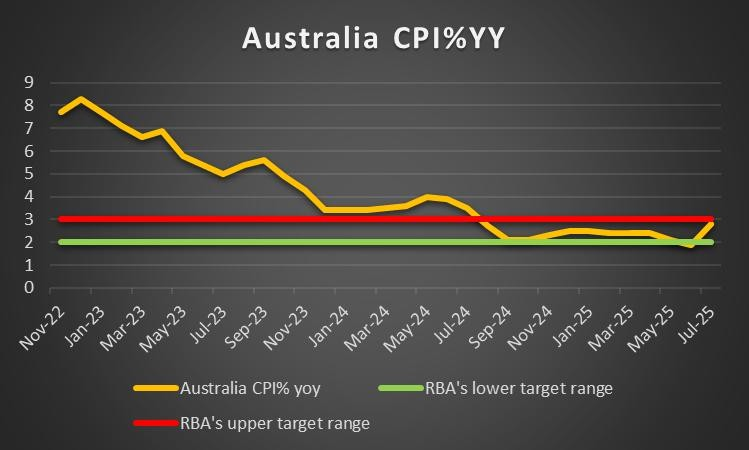

AUD – GDP rate for Q2 due out next week

to a macroeconomic level, Australia’s CPI rate on a month of month level came in hotter than expected implying an acceleration of inflationary pressures which may have aided the Aussie and countered the dovish remarks which may have appeared in the RBA’s last meeting minutes which were released on Monday. For next week Australia’s GDP rate for Q2 is set to be released next week and should it showcase an improvement in the country’s economic growth it may aid the Aussie and vice versa.

Analyst’s opinion (AUD)

“The RBA’s minutes in our opinion where dovish in nature and thus could weigh on the Aussie in the coming week as well. In our view we not be surprised to see a dovish rhetoric emerging from RBA policymakers and for the Aussie to cede control to other stronger currencies.”

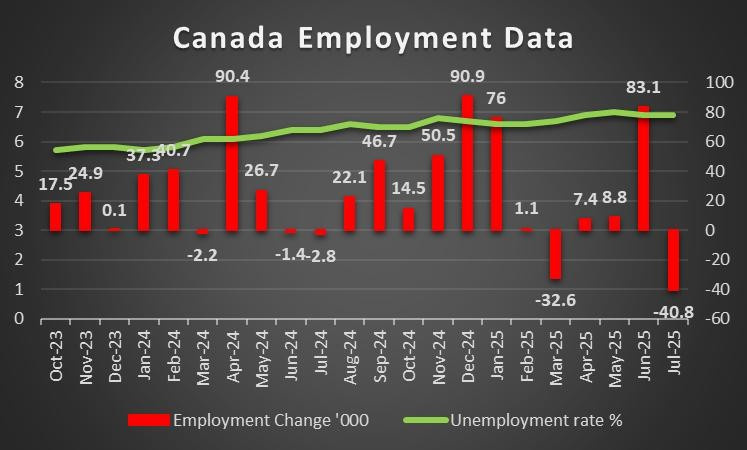

CAD – Canada’s Employment data due next Friday

Loonie traders are expected to be fairly busy with the nation’s employment data set to be released next Friday. Should the employment data for August showcase a resilient labour market it may aid the Loonie, whereas should the data showcase an easing labour market it could prompt the BoC to possible continue on their rate cutting path which may then weigh on the CAD. Furthermore, we would like to note that the Ivey PMI figure for August is set to be released following Canada’s employment data and could either weigh or aid the Aussie depending on the financial release.

Analyst’s opinion (CAD)

“The CAD has some key financial releases due out next week but given that the US Employment data is also due out next Friday it may overshadow Canada’s employment data. Therefore, the narrative from Canada may mitigate or amplify the impact following the release from the US employment data.”

General Comment

In the coming week, we expect the USD to maintain it’s influence over other currencies given the release of the US Employment data. Moreover we would like to note that from the US Equities markets perspective it has been a relatively good week with the S&P500 and NASDAQ 100 ending the week in the green’s whilst the DowJones 30 index is currently in the reds. Furthermore, in Europe, the French equities markets faced downwards pressures following the announcement that France may need to vote for a new Prime Minister thus sending the country into political turmoil once again

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.